The CSS Financial Aid Profile is a secondary financial aid application used by many colleges to award their own financial aid (specifically grants offered by private not-for-profit colleges). The application is required to qualify for institutional grants at those colleges that ask for the form. Since we know that the largest source of grants for college is institutions (colleges and universities), if you are attending one of these colleges that require the CSS Financial Aid Profile, you better make sure it is on your list of forms to complete.

CSS Financial Aid Profile!

So here’s some good news. The CSS Financial Aid Profile has a cost ($25 to register and $16 per school). This can get expensive if you are applying to a lot of colleges that need the CSS Profile, but the College Board has expanded the eligibility for fee waivers. Starting with the 2022-23 CSS Profile, students from families earning less than $100,000 will qualify for free submission, and this will make access to the application much easier for families as they apply for aid.

Here are some resources for you:

The announcement of the fee waiver from the College Board.

The list of colleges which require the CSS Financial Aid Profile.

How did the year go by so fast? Can it almost be October 1 again already?

Phew!

So much has happened in the last year, and Moneyman has been busy with the details of his day job, so apologies for the lack of updates. He promises to do better this year!

As we get ready for another year’s worth of FAFSA updates and changes, it is time to share some resources with you.

Here is a copy of the PowerPoint presentation Moneyman uses when speaking about financial aid to high school students and their parents. Once the video replay is available, we can share that link as well.

Here is a copy of the PowerPoint presentation shared with Florida High School Guidance Counselors by Moneyman and others recently covering a lot of the same information. You can watch a replay of the session here or here.

Feel free to follow along this year. Moneyman (me — that’s me) commits to more frequent updates as things happen this year.

Hey everyone! It’s been a while. How have you been?

I’ve been busy working on getting our students set for the Fall and opening up the application cycle for 2021-22. And as part of that process, being available for presentations and other speaking opportunities about Financial Aid and the FAFSA.

It’s Alive! It’s Alive!!!

So today I have three opportunities for you to make your application process easier this year.

If you want a presentation on the entire Financial Aid Process, you may want to check out a presentation moneyman did on the process for Orange County Public Schools here. This presentation goes through a lot of the information we review on the blog (in fact, during the presentation we point back to the blog at various points). If you need a Spanish language version, you can check one out here (en español aquí).

If you want a step-by-step review of the FAFSA, and want a look at each of the screens, moneyman has you covered as well. Take a look at this video where we review each screen through the FAFSA and give you important instructions on each field.

And finally, don’t forget about FAFSA Frenzy. FAFSA Frenzy is the program that Valencia College offers each year to assist FAFSA filers. This year, their program runs from October 12 to November 13 and has two options: Tuesday nights at 6:00 pm there is a FAFSA presentation, and each Wednesday and Thursday from 9:00 am to 6:00 pm Valencia is offering individual appointments for students and parents to get help on completing the FAFSA. You do not have to be attending Valencia or applying there to make use of this service.

Moneyman hopes your application year goes well. Remember, we are here to answer your questions about the application process, so feel free to ask!

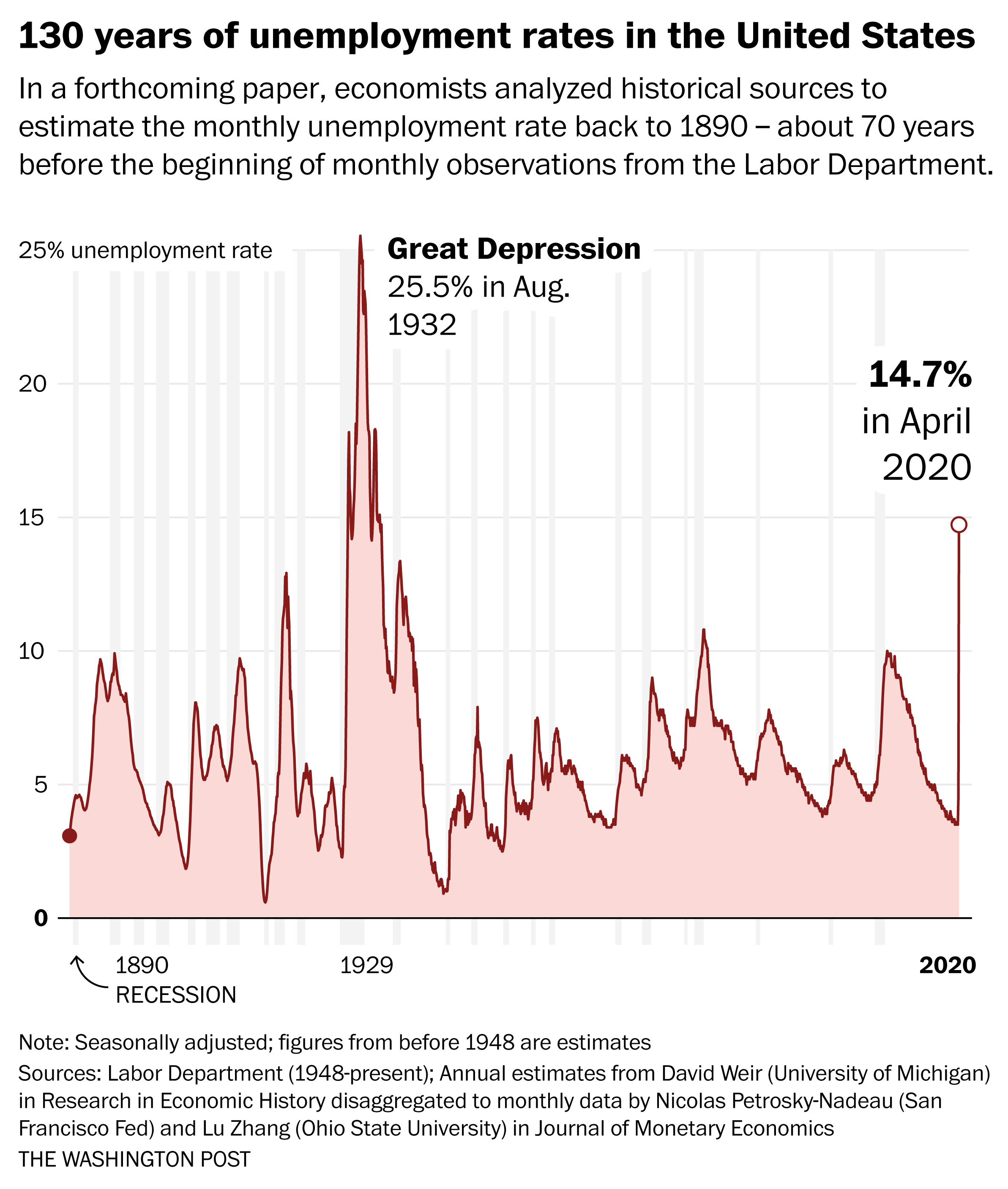

It can be hard to find or keep employment right now. If you are struggling, you aren’t alone. In many ways, this is the worst job market in recent memory, and you can expect that things are going to take a while to recover. Well, what do you do in the meantime? If being unemployed or underemployed isn’t an emergency, then what is?

So we are living through a time which our economy hasn’t seen in more than 90 years. And while the numbers above are an estimate (and don’t reflect the somewhat better news that came with the May report) the general story is still true: lots of Americans who want to work right now cannot. And they need support. Maybe you are one of them. What do you do?

Well, your first step in unemployment insurance. Unemployment insurance was created by states in response to the Social Security Act of 1935 with the idea being that those who have jobs and pay into the system would then be able to draw from the system for retirement and for periods of unemployment. Employers also pay into the system for each employee they hire so that there is a collective coverage of risk. Each state runs their own program, and in this era of COVID-19, the Federal government has added additional limited support for those who have been temporarily furloughed or laid-off during this time. Under these temporary measures, even those who might not have qualified for unemployment benefits in the past (like those self-employed, or independent contractors) might be eligible.

What we’ve all seen is how unprepared many of our state unemployment systems were for the huge numbers of filers who needed to use their system. If you have been stuck, don’t give up. Persistence pays off (as does being up and active on your computer at about 8:00 in the morning, or trying on a Thursday or Friday). Remember also that filing for unemployment is not a one-time thing; you will likely need to log in weekly or every two weeks to refile.

While unemployment can be a helpful tool to cover some expenses during a time of uncertainty, it likely will be of short duration and (without the CARES additional benefit) will most likely leave you short from your previous income. So what’s next?

You may qualify for SNAP. SNAP (or Supplemental Nutritional Assistance Program, often referred to as Food Stamps) is a program to assist with the purchase of food for those who qualify. Again, rules are determined by the state in which you live and you apply using their application. During the COVID-19 pandemic, some states have been increasing the amount of the benefit payments for families with children due to the suspension of many free or reduced school lunch programs.

If you need help with Health Insurance, you may qualify for Medicaid. Medicaid is a program that helps families and individuals with health insurance if they have a low income that qualifies. Medicare is for those who are 65 years of age and older and provides health insurance coverage for qualifying adults. While the names may sound the same, they are very different programs, so make sure you know which one you are trying to obtain.

Once you secure help from the Federal Government and your state or local government, what’s next? Many local charities provide many different kinds of assistance, from food and clothing to shelter and employment. Some schools have updated their web pages to share local resources for assistance (see Valencia College and USF’s Food Panty page as examples).

Emergency situations happen, and if you are still a student enrolled on campus and you need assistance, reach out to Counseling, Advising, or Financial Aid. Chances are that your school has an Emergency Financial Aid program which can help with urgent situations. And make sure you check in to see if you can apply for CARES funds if you haven’t already (and if your school hasn’t already distributed its allocation).

What other resources have you found helpful in the case of emergency? One way to make sure you protect yourself from emergencies in the future is to start a savings plan. Next time we are going to start talking about one of the best ways to save for future spending needs – retirement savings.

The past few days have seen a series of records for highest number of new cases of COVID-19 in Florida. Each day the curve rises, and the picture is fairly clear: we have not yet hit a plateau of cases in Florida.

Source: New York Times (retrieved 6/20/2020)

At the same time, many colleges and universities (in Florida, and indeed all over the country) are beginning to announce their plans for Fall. Among others, UF and FSU have announced plans that will bring students back to campus, although both schools plan to not require students to return to campus in large numbers after Thanksgiving. Other schools, like Stetson University and the University of Tampa, have announced changes to their Fall calendars (either delays in opening, or moving up opening) to allow for a modified Fall semester. And finally, some schools like Valencia College and St. Petersburg College have announced that they will have a very limited number of classes on site in the Fall, and that most classes will remain online.

There are as many colleges and universities as there are plans for reopening. In part this is due to a lack of a clear sense of what’s coming for us in this pandemic, and – at the same time – students seem to be picking up on this confusion. In a recent study conducted by the Florida College Access Network, 42% of current college students surveyed indicated that their plans have changed for their education past high school; some are taking a semester or a year off, some are starting sooner than planned, and some are transferring to another school. At the same time, nearly 1 in 4 parents of high school juniors and seniors indicated that their children’s plans for life after high school have changed: 31% have postponed their plans, 27% have switched to an option closer to home, and 22% have switched to a less expensive option.

At the same time, the survey reveals that those with a high school degree or less are the most impacted by the economic difficulties that have come along with the pandemic. 64% of those with a high school diploma or less reported job loss, pay cuts, or reduced work hours, while at the other extreme, only 50% of those with a bachelor’s degree (and 40% of those with a master’s) reported the same difficulties.

Health insurance is another kind of protection for situations that you aren’t expecting. While we won’t go through every different kind and option of health insurance today (you can read more about all of this here), we do want to look at two options: employer-sponsored health insurance and the Affordable Care Act (also called the ACA or Obama-care).

The law changed in 2010, and children can remain on their parents’ insurance plans until they are 26, so chances are many of you are covered by your parents, but once you turn 26 you will need to find your own coverage.

Generally a health insurance plan will require you to pick a primary care physician. This doctor will coordinate care for you and help you find specialists when more advanced care is required. The benefit of a health insurance plan is that you will have coverage in case things go wrong with your health (without insurance you may have to pay a large amount for your care). The downside of health insurance is that you often can’t just see who you want without getting approval first through your Primary Care doctor.

In addition, many health insurance plans have co-pays, deductibles, co-insurance, and maximum out-of-pocket costs. What are all of these?

A co-pay is the amount you will pay immediately out of pocket to see a doctor or specialist. The amount varies by your plan, but generally runs between $10 and $50 per visit depending on the level of specialty, or could be up to $100 or more for an emergency room visit.

A deductible is the amount of money in total that must be paid for health care services before your insurance covers your expenses. Usually the deductible does not apply to your primary care physician visits but to other types of care.

Co-insurance kicks in after your deductible. This is a percentage of costs that you must pay as your insurance pays the other portion. For example, if your plan has a co-insurance requirement of 20%, then you pay that 20% of the cost and the insurance company pays the other 80%. This will hold true until you pay your out-of-pocket maximum.

An out-of-pocket maximum represents that maximum total cost you will have to pay before your health insurance will cover 100% of any remaining costs for you.

All of these reset each year, so it is important to understand where you are as you plan your care. As an example, let’s say that you are in an accident and require hospitalization for a week. The bill arrives and with medical care, surgery, anesthesia, and all other expenses, the total cost is $110,000. Usually your health insurance has negotiated rates which are better than the regular rates you would get if you walked off the street without insurance, so let’s say this drops immediately to $65,000 because of these negotiated rates. Your insurance has a $100 co-pay for Emergency Rooms, $500 deductible, a 20% co-insurance, and a $5,500 maximum out-of-pocket. Well, you would have to pay the $100 co-pay and then the $500 deductible which is $600. The remaining cost is $64,400 and 20% of that is $12,880 which is way above your maximum out-of-pocket. Since you already paid a $100 co-pay, and a $500 deductible, your maximum additional cost would be $4,900 (your $5,500 max minus $600 already paid). In this case you would have paid a total of $5,500 for the equivalent of $110,000 worth of care. Good thing you had health insurance. In addition, any additional expenses you had for the remainder of your coverage year would be covered at 100% because you have already paid your maximum out-of-pocket for that year; this would all reset the next year when your coverage begins again.

Of course, the other way you pay for insurance is when you pay your monthly premiums. Health insurance is not free although some employers may pay some, part, or all of your monthly costs. If you have an employer-offered health insurance program, chances are that your employer is paying a significant part of the cost for you as a benefit. In addition, any amount you pay as a monthly premium is deducted from your salary prior to paying taxes, so you get to count this as tax-free income.

There are other ways to save money on health care expenses like Health Savings Accounts and Flexible Spending Accounts, and we will cover these at another time.

What if you aren’t working or you want to look at other options? The healthcare.gov site provides information on the plans that are available through the ACA, and could be less based on your income and family size. Take a look because as you know now, we always want to protect ourselves against the unexpected.

Speaking of expecting the unexpected, what is your college or university planning to do regarding reopening? Are you changing your educational plans this fall? Or are you adopting a “wait and see” approach? Moneyman want to know, so clue me by adding your comments at the top of the post!

We are sailing in choppy seas. Between the Coronavirus pandemic, the rising unemployment, civil unrest, and political chaos, it may feel like everything is out of control. Back when moneyman (that’s me!), laid out some themes for this year’s blog entries, this month was envisioned as a focus on “what happens when the unexpected happens.” That was the plan, at least. And then… the unexpected happened.

With that in mind, it is time to tackle some of the subjects which moneyman had planned to discuss in the month of June. Let’s start with life insurance.

You might say, but moneyman I am too young to think about that now. And you would be… completely wrong. The right time to think about life insurance is now, when you are young. Life insurance is the perfect way to plan for the ultimate in unexpected situations. By purchasing life insurance at a young age, you get two important benefits: a much lower monthly rate for your premiums, and the chance to qualify for insurance (hopefully) long before you have developed or suffered from any long-term health complications.

Life insurance is basically a bet on behalf of the companies who provide it. They are betting the likelihood of having to pay out a benefit and they base this generally on your age, gender, smoking status, and health condition. If you seek insurance as a 22 year old who is healthy and doesn’t smoke, your cost is going to much less expensive than that for a 60 year-old smoker with a history of diabetes and cancer.

Also keep in mind that life insurance premiums are monthly payments and the longer the possible length of payments before the company may need to pay out on the insurance, the lower the monthly payment will be. Also the more you ask for in insurance, the higher the monthly payment, so it would not be unreasonable for the same monthly payment to buy much more in insurance coverage for our hypothetical 22 year old above than it would for our 65 year old.

What about the different kinds of life insurance? There are many different kinds of life insurance, but we are going to cover the main two – term insurance and whole life.

Term insurance covers you for a specific period of time, and then ends. Under term insurance you can buy coverage for a specific dollar amount over a specific number of years and as long as you continue to pay the monthly premiums you are covered for the amount you have contracted. One of the downsides of term life insurance coverage is that after the coverage ends, you lose any money you have spent in premiums (so if you don’t use it, you lose it). One of the upsides of term life insurance is that it tends to be pretty inexpensive in comparison to other insurance types.

There is even a special kind of term insurance called permanent life insurance. Like it sounds, this is similar to term life except that the term is forever. So again as long as you pay the premium monthly, you will be covered for the amount you select, but the program never ends until you pass away (or stop paying your premiums). Again, the benefit here is the lower cost (slightly more than term life, but less than whole life). The drawback again is that if you cancel it, you lose your investment.

Then there is whole life insurance. Whole life insurance allows you to make a monthly payment, but there is no expiration date on the insurance. Your monthly payment is invested for you by the insurance company and builds cash value. Yur monthly premum is usually withdrawn form your payment, or is taken as a percentage fee on your earnings, but your investment remains yours. This means you can borrow against this if necessary (for emergencies) or if you cancel your program will receive a cash settlement. When you pass away, your insurance will pay the amount of the death benefit you have chosen minus any outstanding loan amount. This is a great choice if you can afford the monthly premium (which tend to be higher than term life).

It is true that you might earn more in returns if you invest on your own and direct your own investment choices, but for those who do not have time or inclination to make these kinds of decisions, whole life might be a good choice.

So why should you look at life insurance now? And how much should you choose to insure? And should you choose whole or term? This is really dependent on your monthly income and expenses. If you can afford whole life, you can consider your monthly payment into this program as your monthly savings amount as well (because you will eventually be able to access it, one way or another). You want to purchase as much of a death benefit as you can afford, because whatever amount you think you might need now will look very small when you ultimately need it. Imagine that right now you purchase what looks like an unimaginably high $200K death benefit, and then in 8 years you buy a house for $300,000 (right now the average home price in Orlando is $260K). You will kick yourself for not having a higher value when the premiums were cheap. Price it out and see what is affordable!

And don’t forget one other important kind of life insurance; the free kind. When you get hired by an employer ask if one of the benefits of employment is life insurance. Many employers will provide free (or significantly reduced cost) life insurance for you at 1X, 2X, 3X or more than your annual salary. Some employers will even waive the health screening for the higher levels of this insurance, but only if you take the benefit when you first are eligible for it; if you choose to take advantage of this in later years, you may have to go through a health screening first.

If you want to read a lot more about all of the different kinds of life insurance and the pros and cons of each type, check out this Investopedia page which has TONS of good information. Life insurance is the ultimate example of preparing for the unexpected, but we should all be prepared.

Oh, and the best news yet? Like retirement assets (401Ks or IRAs), life insurance plans are ignored as assets on the FAFSA. So you can save lots in your whole life plan, and never have to report it as an asset when you apply for financial aid.

So, Philip J. Fry, pay attention. Jkjk means just kidding on my previous just kidding. And guess what friends? That’s what’s happening with the Student Eligibility rules for CARES Grant funds. The Department of Education just let us know they are about to issue a new rule that says “just kidding” on their previous “just kidding”.

For those of you who might need a refresher, here is where we are so far:

The CARES Act is signed into law by the President on March 27, 2020. As part of the law, the Higher Education Emergency Relief Fund is created, with $12B of relief funds for students. The law is silent on who specifically is eligible for these funds. We first published a review of the act on April 1.

On April 9, the Department publishes the agreements and amounts of funding which would be available under the HEERF. The agreement says that schools “…[retain] discretion to determine the amount of each individual emergency financial aid grant consistent with all applicable laws including non-discrimination laws.” Other than that reference, there is no limitation from the Department on who is eligible for these funds. We covered this on the blog on April 11.

On April 21, the Department issues some FAQs related to the CARES Act at the same time as they issue the agreements for the institutional portion of the funding, and for the first time (in the answer to question 9) mention that students would have to be eligible for Title IV Financial Aid to be eligible to receive HEERF / CARES Grant funds. We covered this on the blog on April 26.

On May 21, the Department says “jk” and issues three paragraphs which says that their previous guidance doesn’t have the force of law, and that while they will enforce the restriction on undocumented students receiving HEERF funds, they will not enforce the restriction on Title IV eligibility. We discussed this on the blog on May 21.

And this brings us to today. As of last night, the Department has indicated that they are about to release an Interim Final Rule in which they will announce that they are planning on enforcing the restrictions on Title IV eligibility effective once the regulations are published in the Federal Register (in other words, “jkjk”).

So where does this leave us? Great question!!

As of the day this is published in the Federal Register, the rule goes into effect. As of that point, schools must follow the rules that state that only students who are or could be eligible for Title IV financial aid (in other words eligible under section 484 of the Higher Education Act) are able to receive HEERF grants. This means that students who are looking for funds will need to file a FAFSA (or if a school chooses to allow it, fill out a self-certification form saying that they meet all eligibility rules).

What are the rules? According to the Interim Final Rule, this includes:

…(1) enroll or be accepted for enrollment in a program leading to a recognized credential at an eligible IHE and not enrolled in elementary or secondary school (2) if presently enrolled, be maintaining satisfactory academic progress (3) not owe a refund on a Federal student grant or be in default on any Federal student loan (4) submit a Statement of Educational Purpose (5) are a U.S. citizen, National or eligible noncitizen (6) not have been convicted of, or plead nolo contendere or guilty to, a crime involving fraud in obtaining federal student aid (7) have a high school diploma or its equivalent (8) have a valid social security number (9) register with the Selective Service (if required) (10) not been convicted of any offense under any Federal or State law involving the possession or sale of a controlled substance for conduct that occurred during a period of enrollment for which the student was receiving Federal student aid.

The largest issue for students may be SAP. We’ve talked about SAP before, but for students who have failed SAP and either didn’t appeal, or didn’t previously apply for financial aid so there was no impact, a bad SAP status could be a deal-breaker for HEERF eligibility. If you are one of these students, you should get a SAP appeal turned in immediately.

The other issue is what constitutes a student. There are two main questions here: are students who graduated or withdrew in Spring still eligible for funds, and are students eligible if they are enrolled in educational programs which are not eligible for financial aid? The answer to the first question is unclear; this was not addressed by the Department in its guidance. The answer to the second question is “no”; the Department clearly says that if your educational program is not eligible, then you aren’t eligible (page 30 reads, “Some programs at title-IV eligible institutions, primarily shorter training courses such as first responder training certificate programs, do not participate. Students enrolled in such programs will not be eligible for the emergency financial aid grants.”).

So where does this leave us? Many schools have already given out the majority of their CARES Funds. Do they have to go back and take it away from anyone they gave it to who might now not be eligible? The good news is a resounding “no” to this question, as long as they restricted the funds to US Citizens and Eligible Non-citizens. The Rule specifies (page 20 footnote 6), “Nor will the Department enforce the title IV eligibility interpretation announced in this rule against distribution of HEERF funds that occurred prior to the publication of this rule.” Keep in mind the publication of the rule is when it appears in the Federal Register so any distribution prior to that point is not subject to enforcement.

So for schools that have already given out most or all of their funds, they do not need to reconsider funds already expended. But for schools that were waiting for guidance, or who have money left to award, we are back to square 1 (or was that square 3 actually).

If you are a student, and you don’t know what to do, check in with your financial aid officer. Search your college’s webpage to see what they have published about their CARES awarding process. But try to be patient with us. The rules have changed yet again, and we are all trying to digest them.

And a final reminder… Until this is actually published in the Federal Register, NOTHING IS FINAL. This is all (you guessed it) subject to change. In other words, watch this space for the “JkJkJk” post.

George Jefferson and Archie Bunker, best frenemies.

George Jefferson was Archie Bunker’s equal in many ways (some might even argue his superior). While no one could call them “friends”, per se, they certainly served as perfect foils for each other: two lovable, obstinate characters, each one proving that stereotypes never holds true when confronted with individual identity. “All in the Family” meets “Moving On Up”. And these shows left lasting memories. And they always showed prejudice and bigotry as the idiocy that it is; both characters always got what they deserved.

Do these sitcoms hold up? Are they worth watching nearly (gasp) 35 to 45 years later? A recreation in 2019 on TV would argue yes (as would Kerry Washington, Jimmy Fallon, Jamie Foxx, Wanda Sykes, Woody Harrelson, among others). These shows were way ahead of their time, or — sadder to say — our times haven’t moved way ahead in the last 40 years, and nothing is more relevant today than confronting the scourge of racism and the terrible conditions faced by BIPOC (Black, Indigenous and People of Color) in our country. We all should dream of a day when shows like “The Jeffersons” and “All in the Family” are viewed as relics of a historical past, barely able to be conceived of, and not simply dated reflections of our present.

With that in mind, “all in the family” carries a different connotation for me for financial aid, and I want to turn there next.

But first, a check in. How are you doing, dear reader? I personally have not been OK. The trauma of the last few weeks has me sad, angry, anxious, depressed, and frankly traumatized. And I am a white, cis-gendered, married man in my 50s who never has been the victim of systemic racism. I know that I am privileged and am here to witness, to listen, to learn, and to act to make change. This is not a political statement, this is a human statement. And I am here to partner with each of you to make change possible.

For me, that means I do all that I can to demystify the financial aid process so that each one of you can find your way into economic opportunity through higher education (and find the best and most cost-effective way to pay for it). We talk about a lot of subjects here, but the most important one is you. I am hoping you are OK. If not, I am here to listen. Contact me by commenting below or using the comment form.

Now to our financial aid subject: “All in the family”. Part of the verification process requires you to document who is in your family. And who will be in college. If you remember back to when you completed the FAFSA, you entered these numbers on the form. If you have been selected for verification, now is the time to provide your list.

Schools will ask you to complete a list of those in your family on the verification form. You will list each person, their relationship to you (the student), their age, and (if they are in college) where they are attending school. For a dependent student, this will mean the members of your parent(s)’ household. You usually will list the parent or parents you live with, if you have step-parents living with you, your siblings or step-siblings who live at the home with you, siblings or step-siblings at college or living elsewhere if your parent(s) provide more than 1/2 of their support, and any other person for whom your custodial parent provides more than 1/2 of their support if they live with you. This might include your grandparents, for example, if they live with you, or your cousin, or aunt, or uncle (if your parents provide more than 1/2 of their financial support each year).

A common mistake people make is assuming that someone has to be listed on your parents’ tax return as a dependent in order for them to be part of your family. This couldn’t be further from the truth; there does not have to be a one-to-one relationship between them. You do want to be prepared, though, to list them on your verification form because if the financial aid officer sees a difference between the number of people in your family on the FAFSA and the number on your verification form, they will want an explanation.

For an independent student, the household size always includes you and (if married) a spouse who is living with you. You can also include your children (even if they don’t live with you) as long as they receive more than 1/2 of their support from you (and your spouse). Finally, you can also claim people who live with you who are not your children if you provide more than 1/2 of their financial support (say an elderly parent or grandparent, or a cousin, or niece / nephew). Remember to list each of these household members on your verification form.

Now we turn to the number in college. If someone in your household plans to attend post-secondary school (college or university) at least half-time, even for one semester, they count as part of your family in college, with one big exception. For dependent students, you cannot count a parent in college. The government assumes (incorrectly in many cases), that parents in college have financial support for their education and are not paying that cost. (This, by the way, is a great example for when you might want to ask for a professional judgment; provide a copy of your parents’ tuition bill for their own education and ask the financial aid office to consider this as a cost when analyzing your EFC). The number in college also does not include students attending a service academy because most of their costs are paid for by the Federal government.

Otherwise anyone who counts as a member of your family could count as part of the number in college. The number in college is important since your PC (Parent Contribution) is divided by this number. For example, if a family has a 12,000 total PC, and two in college, each student would have a 6,000 PC (granting them an additional 6,000 in need each). If there were three in college, the PC for each would be 4,000 and all three students would likely be Pell Grant eligible.

On the verification form, you will be asked to list each college / university attended for each member of the family, and occasionally a school may ask you to have your sibling’s college fill out a form documenting that they really are attending there. Just another way to “trust but verify“.

In closing, while you want to think expansively and include everyone you can in your family list on the verification, you want to make sure you can document the folks you choose. In short, you want to make sure you keep it “all in the family”.

Here’s hoping and praying for change to come soon. In the words of James Taylor (in his song Shed a Little Light):

Shed a Little Light

There is a feeling like the clenching of the fist There is a hunger in the center of the chest There is a passage through the darkness and the mist Though the body sleeps the heart will never restOh let us turn our thoughts today to Martin Luther King And recognize that there are ties between us All men and women, living on the earth Ties of hope and love, sister and brotherhood That we are bound together With a desire to see the world become A place in which our children can grow free and strong We are bound together by the task that ties before us And the road that lies ahead, we are bound and we are bound

Let’s face it. Verification isn’t fun. When you are selected for verification, it can feel like a burden, and it may feel like those of us who are working in financial aid are trying to “get into your business”. Trust moneyman, it isn’t our choice. If you are selected for verification it might feel like the flip of a coin at random (heads or tails?), but once you have been selected there are certain principles we need to follow.

Flip a coin… See where it lands…

One of these principles is that while financial aid officers are not accountants, we do need to know some basic tax information. Federal Student Aid publishes an annual Application and Verification Guide for financial aid administrators (which is very technical, feel free to read it if you have nothing better to do) which perhaps says it best:

Financial aid administrators do not need to be tax experts, yet there are some issues that even a layperson with basic tax law information can evaluate. Because conflicting data often involve such information, FAAs must have a fundamental understanding of relevant tax issues that can considerably affect the need analysis. You are obligated to know (1) whether a person was required to file a tax return and (2) what the correct filing status for a person should be.

Page 132 of the 2020-21 AVG

So here we go. Let’s start with Heads… In this case, Heads of Household.

If moneyman sees one common mistake that holds up families from completing verification, it is both parents filing their tax returns as head of household even though they are married and living together. The rules for filing Head of Household (as published by the IRS) say:

“You may be able to file as head of household if you meet all the following requirements:

You are unmarried or “considered unmarried” on the last day of the year…

You paid more than half of the cost of keeping up a home for the year.

A qualifying person lived with you in the home for more than half the year (except for temporary absences, such as school). However, if the qualifying person is your dependent parent, he or she doesn’t have to live with you. See Special rule for parent, later, under Qualifying Person.”

If two parents file as married on the FAFSA as their marital status and then provide separate tax returns with one or both filing as Head of Household, this is usually a problem. To correct this, the family either needs to prove that they meet the qualifications above, or they need to file an Amended Tax Return. Otherwise we cannot complete verification.

Why would a family want to file as Head of Household? Usually tax rates are lower, so amending a return may mean that the family needs to pay more in taxes, but to qualify for aid it is necessary to resolve this discrepancy. There could be a possible reason for a parent to file Head of Household on a tax return (say for the 2018 tax return), but file the FAFSA as “married” for 2020-21, but the situation is unlikely. Lots of examples (and much more detail) can be found at this link.

More T(r)ials (or trials) of verification:

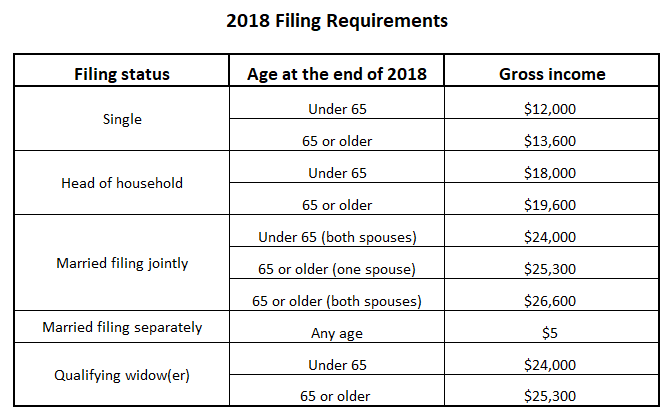

The quote above also mentions that financial aid administrators should kow if a parent or student should have filed a tax return (if they earned enough income to be required to do so).

How does this work? The same IRS publication lists the minimum income thresholds which require a taxpayer to file a Federal income tax return.

According to the chart, if a regularly employed (not self-employed) individual earns above 12,000 (and they are single and under 65), they must file a tax return. Of course, a taxpayer might choose to file anyway so that they can get their tax refund, but the above chart represents the numbers of income at which you must file a return. Note (by the way) that spouses who file separately have a very low income threshold – only $5.

Self-employed individuals have even a lower threshold. If you are self-employed and your net earnings are greater than $400, you need to complete a tax return.

Sometimes we hear from students whose parents do not file a tax return because they don’t believe they have to. In these cases, we are required to collect copies of W-2s, and “non-filer” from the IRS to show that the taxpayer did not file a tax return. But if the income is above the minimum income threshold, we must have a tax return.

Here are the trials of verification. What stories have you experienced? Where do you get hung up in verification?

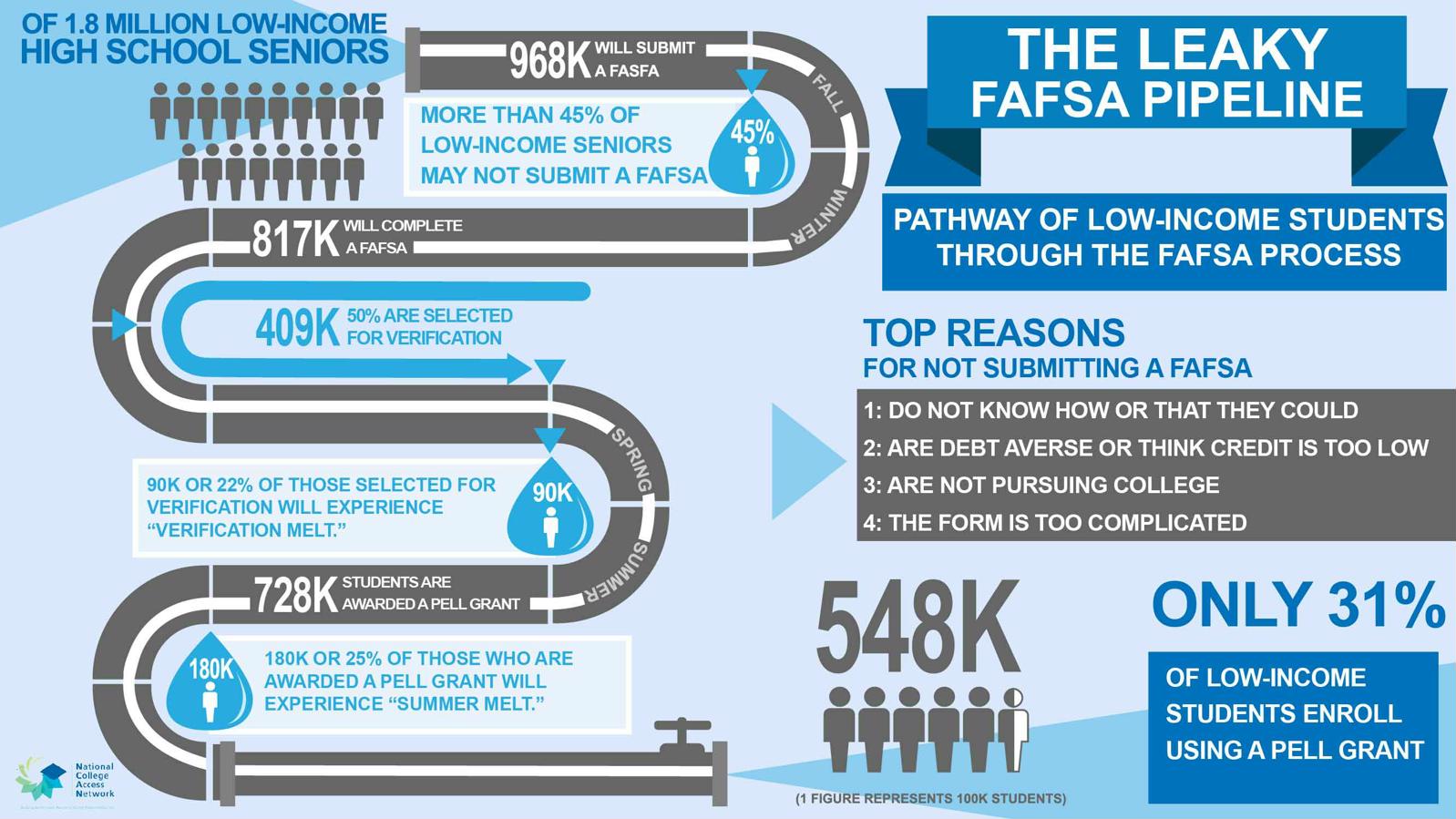

NCAN (the National College Attainment Network) in 2017 published a study of the leaky FAFSA pipeline. According to their study, 22% of applications selected for verification drop out due to the difficulty of the process.

Don’t be part of the melt! Ask your verification question here and moneyman will help!! Don’t leave your financial aid unclaimed! Be “cool” (don’t be part of the summer melt) and don’t “flip”!

So not everything you read on the Internet is true. I know. Shocker.

Yoda, Kermit, it’s all the same…

Some things on the Internet need to be taken with a fair amount of disbelief. Almost an approach of “trust, but verify“.

So I can understand if you might not believe what I am about to tell you when it relates to the HEERF Funds from the CARES Grant. There is a lot of information on the Internet! And a lot of it is true! (Or as true as the most recent update).

Colleges and universities are required by the Department of Education to provide updates 30 days after receiving HEERF Funds and every 45 days thereafter. According to guidance issued by Federal Student Aid on May 6, 2020, colleges must post the following information to their publicly facing websites within 30 days of receiving their funds:

An acknowledgement that the institution signed and returned to the Department the Certification and Agreement and the assurance that the institution has used, or intends to use, no less than 50 percent of the funds received under Section 18004(a)(1) of the CARES Act to provide Emergency Financial Aid Grants to students.

The total amount of funds that the institution will receive or has received from the Department pursuant to the institution’s Certification and Agreement [for] Emergency Financial Aid Grants to Students.

The total amount of Emergency Financial Aid Grants distributed to students under Section 18004(a)(1) of the CARES Act as of the date of submission (i.e., as of the 30-day Report and every 45 days thereafter).

The estimated total number of students at the institution eligible to participate in programs under Section 484 in Title IV of the Higher Education Act of 1965 and thus eligible to receive Emergency Financial Aid Grants to students under Section 18004(a)(1) of the CARES Act.

The total number of students who have received an Emergency Financial Aid Grant to students under Section 18004(a)(1) of the CARES Act.

The method(s) used by the institution to determine which students receive Emergency Financial Aid Grants and how much they would receive under Section 18004(a)(1) of the CARES Act.

Any instructions, directions, or guidance provided by the institution to students concerning the Emergency Financial Aid Grants.

For you as students this represents finally an opportunity for you to learn exactly how your school plans to spend its CARES Grant allocation. It is information you can believe from the Internet.

For example, if you are a student at UCF, you can see from the University of Central Florida’s website that their application period closed on May 19, and that they plan on awarding funds based on the 21,669 applications received. UCF is awarding different amounts to Pell eligible students vs. non-Pell eligible, and to date (5/23/2020), they have awarded $0.

On the other hand, Valencia College’s CARES Grant page shows that their application window opens tomorrow (June 1) for the approximately 28,000 students who will be eligible for CARES funds. Valencia is requiring a FAFSA and is awarding students for both Spring and Summer terms. Valencia is also requiring an application for funds.

Rollins College has already distributed its entire CARES Grant allocation according to their webpage. Their awards ranged from $500 to $3,000 per student.

So if you are curious to learn how your college is giving away their CARES Act money, then do a search on their web page for “CARES Grant” or “CARES Act”. You will undoubtedly learn some interesting information about how the process is working for your school.

As a matter of public interest, moneyman has started a Google Doc with a list of colleges and universities and their website for CARES reporting. Feel free to add your college or search for a college or university’s page there.