The CSS Financial Aid Profile is a secondary financial aid application used by many colleges to award their own financial aid (specifically grants offered by private not-for-profit colleges). The application is required to qualify for institutional grants at those colleges that ask for the form. Since we know that the largest source of grants for college is institutions (colleges and universities), if you are attending one of these colleges that require the CSS Financial Aid Profile, you better make sure it is on your list of forms to complete.

CSS Financial Aid Profile!

So here’s some good news. The CSS Financial Aid Profile has a cost ($25 to register and $16 per school). This can get expensive if you are applying to a lot of colleges that need the CSS Profile, but the College Board has expanded the eligibility for fee waivers. Starting with the 2022-23 CSS Profile, students from families earning less than $100,000 will qualify for free submission, and this will make access to the application much easier for families as they apply for aid.

Here are some resources for you:

The announcement of the fee waiver from the College Board.

The list of colleges which require the CSS Financial Aid Profile.

How did the year go by so fast? Can it almost be October 1 again already?

Phew!

So much has happened in the last year, and Moneyman has been busy with the details of his day job, so apologies for the lack of updates. He promises to do better this year!

As we get ready for another year’s worth of FAFSA updates and changes, it is time to share some resources with you.

Here is a copy of the PowerPoint presentation Moneyman uses when speaking about financial aid to high school students and their parents. Once the video replay is available, we can share that link as well.

Here is a copy of the PowerPoint presentation shared with Florida High School Guidance Counselors by Moneyman and others recently covering a lot of the same information. You can watch a replay of the session here or here.

Feel free to follow along this year. Moneyman (me — that’s me) commits to more frequent updates as things happen this year.

Hey everyone! It’s been a while. How have you been?

I’ve been busy working on getting our students set for the Fall and opening up the application cycle for 2021-22. And as part of that process, being available for presentations and other speaking opportunities about Financial Aid and the FAFSA.

It’s Alive! It’s Alive!!!

So today I have three opportunities for you to make your application process easier this year.

If you want a presentation on the entire Financial Aid Process, you may want to check out a presentation moneyman did on the process for Orange County Public Schools here. This presentation goes through a lot of the information we review on the blog (in fact, during the presentation we point back to the blog at various points). If you need a Spanish language version, you can check one out here (en español aquí).

If you want a step-by-step review of the FAFSA, and want a look at each of the screens, moneyman has you covered as well. Take a look at this video where we review each screen through the FAFSA and give you important instructions on each field.

And finally, don’t forget about FAFSA Frenzy. FAFSA Frenzy is the program that Valencia College offers each year to assist FAFSA filers. This year, their program runs from October 12 to November 13 and has two options: Tuesday nights at 6:00 pm there is a FAFSA presentation, and each Wednesday and Thursday from 9:00 am to 6:00 pm Valencia is offering individual appointments for students and parents to get help on completing the FAFSA. You do not have to be attending Valencia or applying there to make use of this service.

Moneyman hopes your application year goes well. Remember, we are here to answer your questions about the application process, so feel free to ask!

Let’s face it. Verification isn’t fun. When you are selected for verification, it can feel like a burden, and it may feel like those of us who are working in financial aid are trying to “get into your business”. Trust moneyman, it isn’t our choice. If you are selected for verification it might feel like the flip of a coin at random (heads or tails?), but once you have been selected there are certain principles we need to follow.

Flip a coin… See where it lands…

One of these principles is that while financial aid officers are not accountants, we do need to know some basic tax information. Federal Student Aid publishes an annual Application and Verification Guide for financial aid administrators (which is very technical, feel free to read it if you have nothing better to do) which perhaps says it best:

Financial aid administrators do not need to be tax experts, yet there are some issues that even a layperson with basic tax law information can evaluate. Because conflicting data often involve such information, FAAs must have a fundamental understanding of relevant tax issues that can considerably affect the need analysis. You are obligated to know (1) whether a person was required to file a tax return and (2) what the correct filing status for a person should be.

Page 132 of the 2020-21 AVG

So here we go. Let’s start with Heads… In this case, Heads of Household.

If moneyman sees one common mistake that holds up families from completing verification, it is both parents filing their tax returns as head of household even though they are married and living together. The rules for filing Head of Household (as published by the IRS) say:

“You may be able to file as head of household if you meet all the following requirements:

You are unmarried or “considered unmarried” on the last day of the year…

You paid more than half of the cost of keeping up a home for the year.

A qualifying person lived with you in the home for more than half the year (except for temporary absences, such as school). However, if the qualifying person is your dependent parent, he or she doesn’t have to live with you. See Special rule for parent, later, under Qualifying Person.”

If two parents file as married on the FAFSA as their marital status and then provide separate tax returns with one or both filing as Head of Household, this is usually a problem. To correct this, the family either needs to prove that they meet the qualifications above, or they need to file an Amended Tax Return. Otherwise we cannot complete verification.

Why would a family want to file as Head of Household? Usually tax rates are lower, so amending a return may mean that the family needs to pay more in taxes, but to qualify for aid it is necessary to resolve this discrepancy. There could be a possible reason for a parent to file Head of Household on a tax return (say for the 2018 tax return), but file the FAFSA as “married” for 2020-21, but the situation is unlikely. Lots of examples (and much more detail) can be found at this link.

More T(r)ials (or trials) of verification:

The quote above also mentions that financial aid administrators should kow if a parent or student should have filed a tax return (if they earned enough income to be required to do so).

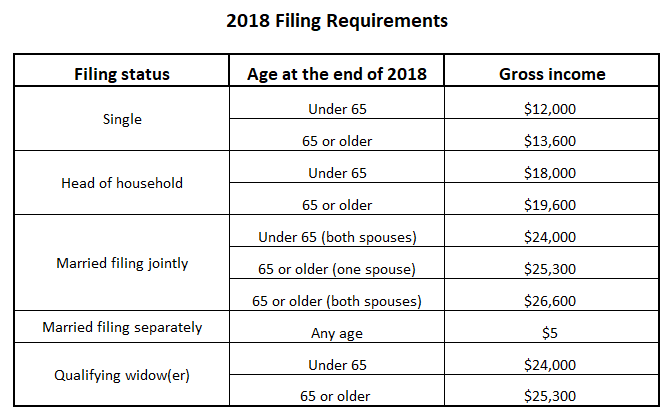

How does this work? The same IRS publication lists the minimum income thresholds which require a taxpayer to file a Federal income tax return.

According to the chart, if a regularly employed (not self-employed) individual earns above 12,000 (and they are single and under 65), they must file a tax return. Of course, a taxpayer might choose to file anyway so that they can get their tax refund, but the above chart represents the numbers of income at which you must file a return. Note (by the way) that spouses who file separately have a very low income threshold – only $5.

Self-employed individuals have even a lower threshold. If you are self-employed and your net earnings are greater than $400, you need to complete a tax return.

Sometimes we hear from students whose parents do not file a tax return because they don’t believe they have to. In these cases, we are required to collect copies of W-2s, and “non-filer” from the IRS to show that the taxpayer did not file a tax return. But if the income is above the minimum income threshold, we must have a tax return.

Here are the trials of verification. What stories have you experienced? Where do you get hung up in verification?

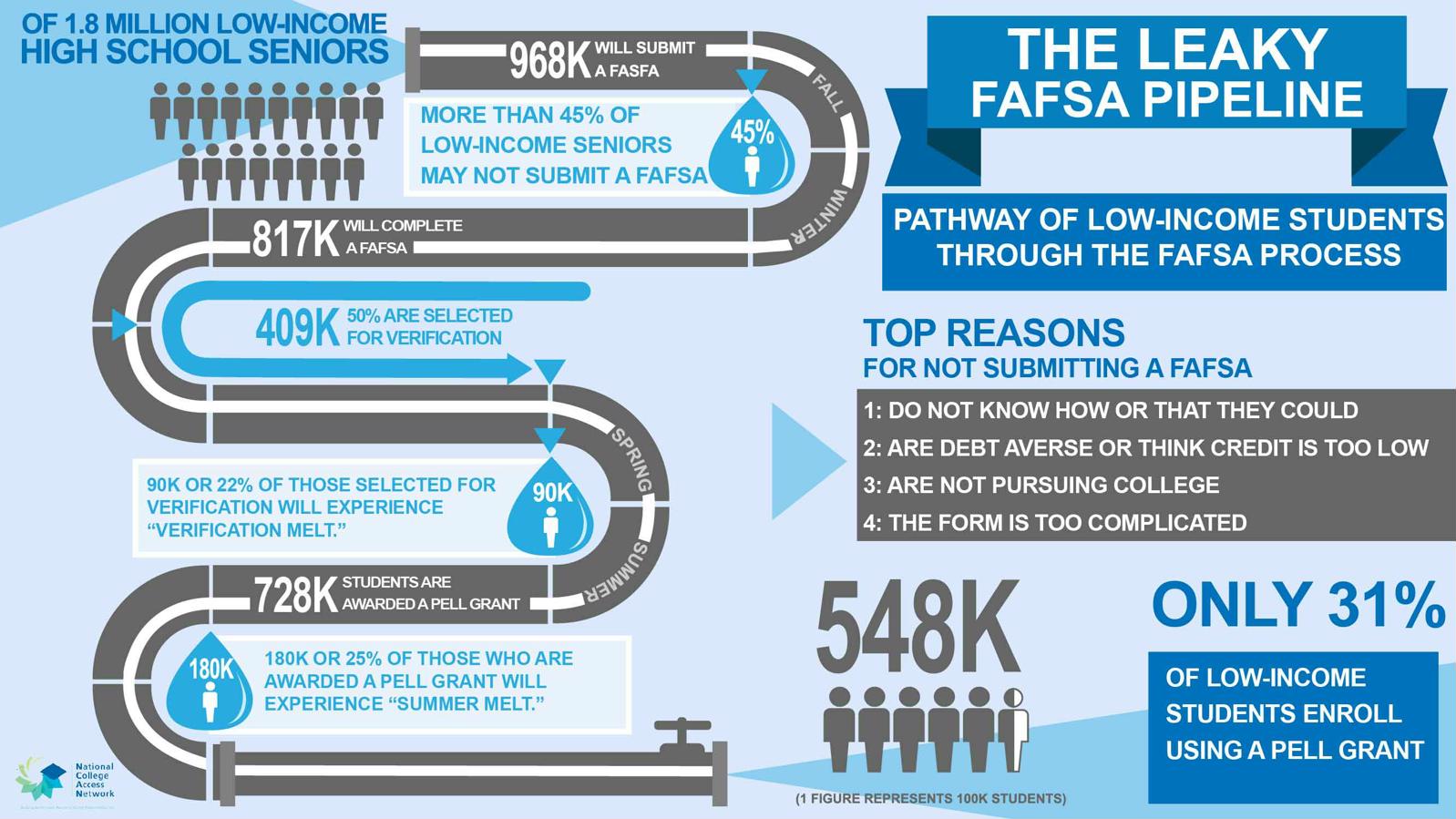

NCAN (the National College Attainment Network) in 2017 published a study of the leaky FAFSA pipeline. According to their study, 22% of applications selected for verification drop out due to the difficulty of the process.

Don’t be part of the melt! Ask your verification question here and moneyman will help!! Don’t leave your financial aid unclaimed! Be “cool” (don’t be part of the summer melt) and don’t “flip”!

“Trust, but verify“. Or in Russian, “Doveryáy, no proveryáy.” It rhymes in Russian. Cute, huh? But where does it come from?

This expression, popularized by Ronald Reagan in the context of nuclear disarmament talks with the Russians, has become a reference to being willing to believe what someone (with qualifications – namely checking to make sure it is the truth).

You could say that the same principle exists within Financial Aid as well. Federal Student Aid trusts, but verifies. They call this process “verification.”

What is moneyman talking about? When you complete the FAFSA, you enter information used to calculate your eligibility for financial aid (your EFC) such as your income, your federal taxes, the number of members of your family, and the number in college (among other items). Remember, your income is based on the last tax year available before the application year opens (so the 2020-21 application year opens on October 1, 2019, so the last tax year available at that time is 2018). Your personal information like marital status (of you and your parents), your assets and your family size on the other hand are as of the date you fill out the FAFSA.

The FAFSA takes the information provided by you and using the formula moneyman has described on this blog, comes up with your expected family contribution which determines if you qualify for a Pell grant and is used in the awarding of other need-based financial aid. But how do we know that the information you provided on the FAFSA is accurate?

Welcome to “doveryáy, no proveryáy“. While the FAFSA trusts you to enter the information, a number of applications (generally not to exceed 30% of those who apply) are selected by the government to go through a process called verification. It is a way of proving what you answered on the FAFSA by providing additional information.

When you are completing the FAFSA you have the opportunity to link your tax information directly to the FAFSA using the IRS Data Retrieval Tool (or DRT). The DRT allows Federal taxpayers to import data directly from the IRS system and answer the associated FAFSA questions. This makes the process of completing the application much easier and faster.

As an additional benefit, if you use the IRS DRT you do not have to verify your income information from another source since you have already done so by transferring information over. If you did not link your application to the IRS DRT, and you are selected for verification, you will need to provide a copy of either your Federal Tax Return transcript (available from irs.gov) or a signed copy of your paper Federal Tax Return.

How do you verify information other than taxes and income? If you re selected, colleges and universities will provide you with a verification form which you must complete to prove the information you filed on the FAFSA. If there are differences between the two sources of information, the school may contact you and ask you to explain the difference. These forms often additionally ask for untaxed income since much of that information cannot be determined from a copy of your tax return.

There is one additional type of verification for which you may be selected, and that is when you are asked to provide your identity by providing documents including proof of citizenship and high school graduation, as well as indicating that you understand that the financial aid you are receiving is for an educational purpose. This is done through another form also provided by your financial aid office.

Some schools (especially those who have a lot of their own grant or scholarship funds to distribute) may select all of their students to go through verification. This is usually because they want to be sure that the amount of funds they provide to students (which is often much more than that provided by the Federal government) is given to those who need the funding. Remember, “trust but verify.”

Verification tends to be a stumbling block for a number of student financial aid applicants. We will explore why in some coming posts, but keep in mind this generally is a requirement of Federal Student Aid and it is just a way to confirm the information provided on your financial aid applications.

“Graduate school? Really? But I just finished my undergraduate degree and now you want me to keep on going? Moneyman, what are you thinking?”

Great questions. And I’m here to answer them. Also the ones you didn’t ask: “How am I going to pay for it?” and “Shouldn’t I go out in the workforce first before I go on to graduate school?”

The choice is yours. Sort of…

In our current economic situation, some of you may be thinking that going on to graduate school after you finish your undergraduate degree is a good choice, and moneyman isn’t going to argue that! Especially if your chosen field is one where advanced degrees are a requirement for later promotions or for entry level interviews, a graduate degree now may be a wise investment.

If we look at data from the BLS (Bureau of Labor Statistics), we can see that a graduate degree pays off (on average) in two ways: increased weekly earnings, and lower unemployment. In fact, in 2019 the income difference between an undergraduate and a master’s degree was $236 per week (or about $12,300 a year). The difference is much higher for a professional degree, like a Law Degree or MD (an average of $686 more per week than an undergrad, or a total of $35,700 per year). Again these are only averages, but they are important to understand the financial potential impact of graduate education.

So if you want to go “back” to school to get your graduate degree, what should expect when it comes time to pay for it? Well, first, let me introduce you to an old friend — the FAFSA. The same form you have been using to apply for financial aid as an undergraduate is also required from you as a graduate student with a few important differences.

You are automatically independent when you apply for financial aid as a graduate student. Even if you aren’t yet 24 years old, your FAFSA can be completed without parental information when you apply for graduate school financial aid (BUT — here is a warning — some law schools and medical schools may ask you to fill in the parental information anyway so that they can use this information to determine if you qualify for their scholarships).

Your application for Federal financial aid will be for loans. The Federal government does not offer any widespread graduate scholarships (like the Pell Grant for undergraduates). Mostly you will do the FAFSA as the first step in qualifying for your Federal loans.

Check to see if your graduate school requires any other financial aid application, either one of their own or using a third-party application system. If they do, fill it out since this may qualify you for scholarship or grant money.

You can likely pick up where I am going here. For graduate school, much of the money available is loans. In fact, you can take a look at Sallie Mae’s report on How America Pays for Graduate School and see that (at least in 2017) about 53% of graduate school costs were covered by student borrowing. The College Board’s Trends in Student Aid 2019 places the percentage paid through loans slightly higher (at 66%).

But what if you want to minimize loans? Well, there is some better news here. Both the College Board and Sallie Mae agree; there is some grant and scholarship money available here (between 15 and 21%). Generally though these scholarships are based on merit and not need. In addition, some of these grants-in-aid may come with requirements for work (like teaching assistantships who lead undergraduate study groups as TAs, or research assistantships where graduate students serve as lab assistants or research fellows). Departments in graduate schools also often have funding sources of their own, so be sure to check with your department head (or better yet their administrative assistant) to see what other funding options are available.

As an example, take a look at UF’s and FIU’s webpages for graduate financial aid and you will see that they match the processes outlined above. And don’t forget the good advice moneyman offered you about private scholarships. Many private funders support graduate education, so make sure to apply for these opportunities.

There is no reason to put off graduate school, especially if you don’t have great luck right now in the job market. Of course, if you are working you also want to take a look at your employer’s benefit package — do they offer graduate school tuition for free? For example, Disney’s Aspire program offers free graduate degrees in a number of career pathways for hourly cast members (and the benefit is even extended during the current closure and furlough). Don’t forget that another great employer may be the university itself (and often tuition reimbursement or remission is a benefit of employment).

What questions about financial aid in graduate school are left unanswered? Let moneyman know by asking a question in the chat.

For many of you, final grades are in and the Spring semester has ended (in fact, some of you may already enrolled in Summer classes). Hopefully your Spring grade were what you wanted them to be and you are looking at a great end to your semester.

Pass the New Grading Options, please!

I recognize though that some of you may have had a difficult semester, especially with classes moving completely online, the changes in living and working situations, and the need to return home from your campus.

Your completion rate (Federally required to be 66.67% or above).

Your cumulative GPA (required to be 2.00 or better).

Your maximum timeframe (150% of the number of credit required for the degree program you are pursuing).

Also remember that if you were already on Financial Aid Warning or working under a Financial Aid Academic Plan while on Probation, you may find yourself with a need to appeal this semester because of your academic difficulties. In a previous post on the CARES Act, I indicated that this semester the Federal Government has offered an opportunity for colleges to ignore classes for which you withdrew if the reason was related to the pandemic. There has been no final guidance offered from the Feds on this yet however so if you withdrew from classes this semester and you are now on a negative SAP status (like Suspension), I would advise speaking to your financial aid officer and letting them know about the CARES Act exemption.

Even if you didn’t withdraw from classes, this is definitely a semester to write an appeal for consideration from the consequences of negative SAP. If your school processes appeals, they can let you know how they prefer these forms or letters to be submitted (ask them or look on their web page), but don’t give up! Of all times, we understand this last semester was tough on you; it was tough on all of us!

The COLA

I also wanted to share a little more advice in this post for those of you looking at post-graduation jobs. With the recent April jobs report showing losses in every part of the job market, it may seem like the most difficult time to be looking for work. That may be true, but the national story is not the story of every part of the country. State and local metro unemployment rates (not yet updated for April) show that different parts of the country have differences in their experience of job losses.

Graduation from college is a time in your life where you can reinvent yourself; this may be the time to think about moving to a new part of the country, or even a different part of the state. You may want to think about relocating to a major city or metro so you can experience urban life if you haven’t done so before, or you may want to try something different than your big city and find someplace more suburban or rural.

Before you run off to start your new life, though, you want to make sure you understand the difference in COLA!

No, not these kinds of COLA

When I say “COLA”, I mean a Cost of Living Adjustment. Think about it this way: a $30,000 income is very different if you earn that in Pensacola, FL vs. Manhattan (NYC), NY. In fact, to maintain the same lifestyle in New York City you would need to earn slightly more than $78,000 (more than twice as much).

Why is that? Well groceries, housing, taxes, transportation, health care – it’s all more expensive in New York City. You may have intuitively known that, but how do you put a number behind that analysis?

Here is where I can help. There are lots of great calculators online that can help you figure this out. Try CNN’s, or the one at Nerd Wallet, or if you know the area of work you want to do, you may want to try this one at salary.com.

Just don’t forget that costs matter. As you are comparing salary offers and trying to decide whether a move to a new city is worthwhile, check the COLA.

Upcoming Plans

Just a reminder that we have a few more topics in our exploration of life after college! Coming up in the next posts: applying for financial aid as a graduate student, creating a post-college budget, and managing those “adult” things — like an apartment lease, car loan, etc.

Feel free to post your questions and suggestions. I’m here for you!

IMPORTANT NOTE: The guidance in this post was contradicted by later guidance from the Department of Education. See herefor the most recent guidance. This post is left as it was originally published for historical purposes.

As in, when will the money from the CARES Act (which I discussed here) and how will students apply for it and receive it?

Well, your friend moneyman has some answers, and lots of questions. Here goes!

On Thursday afternoon, Secretary of Education, Betsy DeVos, released a letter to college presidents (and copied to Directors of Financial Aid and Chief Financial Officers) nationwide explaining that the Department of Education was putting a priority on delivering 1/2 of the Emergency Stabilization Funds that were promised by the CARES Act to schools. Which half? The half that is going to students!

If you remember, this money has to be spent on students to help with expenses related to their education moving online (from the Act – “…expenses related to the disruption of campus operations due to coronavirus (including eligible expenses under a student’s cost of attendance, such as food, housing, course materials, technology, health care, and child care).”)

So how much will colleges receive? Take a look at the list provided by the Department of Education to find your school to see how much your school is receiving (and remember that the list is in school code order). The list shows both the total allocation as well as the amount specifically for students. If you are interested to see how these amounts were calculated, you can find the answer here.

The amounts are large here, but what does it mean for an individual student? So while the agreements that schools have to sign to receive this money (and the money will be available as soon as Wednesday) are also published, there are very few limitations on how the school can award this money.

For example, students don’t have to file a FAFSA to qualify. You don’t have to show financial need, and you don’t even need to be a US Citizen (or Permanent Resident). These funds can be awarded by schools to any attending student therefore, and in addition any amount awarded doesn’t have to follow the normal rules for overaward (or scholarship displacement). So the money gets to go straight to the student and will have no impact on other financial aid.

There is also no limit or requirement placed on the amount of the award which a school can make for a student (although the Secretary recommends no more than the Pell Grant maximum – currently $6,195). The funds must be spent by the college within one year of the date they sign the acknowledgement form.

So to go back to the main question, how do students apply for these funds?

The Secretary doesn’t specify and schools can choose their own process. Schools can also decide how they want to apply these funds (tuition, technology costs, fees, textbooks, etc). This means that for students you are going to need to speak with your individual financial aid office to find out how they are planning on offering this aid, and that there may be a delay while your school figures it out.

At moneyman’s college we are carefully examining the rules and options for these funds and will probably have a combination of some kind of online application for funds, and some categories where we will automatically award funds to students. We will hope to have some decisions in the next week.

So if you are a student, and you need some emergency funds, moneyman’s best advice right now is to be in touch with your school’s financial aid office and let them know that you have need for funds. Ask if you can be placed on a waiting list, or if there is some kind of application you can add your name to. There will be more information coming from your school, you can be sure!!

In the meantime, what other questions do you have?

Right now I’m going to guess that almost everyone who can is spending a lot more time in their “casual clothes”. So I’m not talking about those heroes of this new world we live in — the nurses, doctors, EMTs, grocery store workers, mail carriers, etc. — who still have to leave the house to go to work. But for many of us who can either stay at home to work, or for whom (unfortunately) work is not an option right now, I imagine our dressing patterns have changed.

In fact, the Washington Post recently featured a story they entitled “Business on top; pajamas underneath” all about the move to much more casual “work” attire.

Credit to @calebwallace_17 on Twitter

So maybe it isn’t PJs, but it counts.

Today what counts for this post is a financial aid PJ. And, no, I am not talking about money-themed bedwear, but rather what we call in financial aid a “Professional Judgment”.

When you apply for financial aid, you always use the income from the prior–prior year (so if you apply for the 2020-21 academic year, we use your income from 2018). Why is that, you ask? Well (I answer), remember that the FAFSA “goes live” as of October 1 the year prior to the start of the academic year (in this case, October 1, 2019) and we have to use the last completed income year as of the date the FAFSA goes live (which in this case would be the 2018 income tax year). [I wrote about the FAFSA in a previous post that will give you an overview of the form.]

So to visualize this, it might help to use the image below. You can see that the income you (and your parents?) earned from January to December 2018, for which you filed a tax return in April 2019, and then filed a FAFSA as early as October 1, 2019, is finally used to determine your financial aid for the 2020-21 academic year (with bills usually due in late Summer 2020 and early winter 2021).

The Application Cycle

So the income determining your financial aid earned as long ago as January 2018 can be used to determine the financial aid 20 months later (August 2020)? What? (insert screeching sound here) But what if your income has changed since then? What if you are unemployed or if (heaven forbid) a parent has passed away? What happens then?

Put on your pajamas, grab a snack, and let’s talk about PJs (Professional Judgments).

But first one more aside. There are lots of different kinds of Financial Aid Professional Judgments and we’ve reviewed one of them already here on the blog. When a student is otherwise dependent on their parent(s) for financial aid purposes (see the review of that here), there may be extenuating circumstances that convince a financial aid officer to declare the student independent (more on that process here). This is a kind of professional judgment (relying on the financial aid officer to determine if your circumstances warrant an override of the official definition of dependence) and financial aid officers have many other kinds of professional judgment they are granted.

Another kind of PJ (professional judgment) applies to the situation when a family has lost income (perhaps due to unemployment or to the death of a parent). While the FAFSA requires an analysis of 12 months of income, a financial aid officer is allowed to choose (in exceptional circumstances, and on a case by case basis) a different 12 months if the family’s situation calls for it.

So for example, if a family files the 2020-21 FAFSA using their 2018 income, but a parent loses a job in June 2019, the financial aid officer could use the 2019 income, the expected 2020 income, or the income from June 1, 2019 to May 31, 2020 (or indeed any other 12 month period they thought was appropriate). This flexibility is an option for financial aid officer (never a mandate) and each financial aid officer may make a different decision based on their professional judgment. But there are a few common attributes which, as a student or parent, you should know:

The decision must be made on a case-by-case basis. For example, a financial aid officer cannot say that every one who lost a job due to the COVID-19 situation will be granted an override, but she could review each case one at a time and reach the same decision for each.

The decision must be based on adequate documentation. The definition of adequate is left to the financial aid officer but almost always requires submission of information from a family documenting the condition which caused the request. This might include a notice of termination (job), unemployment compensation forms, a doctor’s note, or a death certificate. Again, the requirements can vary from officer to officer, although most will ask for a letter from the family explaining the situation and some type of third-party documentation.

There is no mandate that a PJ be offered, but Federal Student Aid does encourage those of us in the financial aid offices across the country to take into account the situations many of our families are experiencing during difficult times.

Financial aid officers are not limited to just changing income information when they make a PJ on the FAFSA. Indeed they can override any data element on the FAFSA (and sometimes do) as a response to a family’s special circumstances (they cannot however change the EFC formula). Here are some examples I have seen:

Overriding a family’s cash/savings/checking amount when a family has sold a primary residence but hasn’t yet purchased a new one (remember that the value of a home is not reported on the FAFSA).

Adding to Federal Taxes paid to reflect a family’s additional medical expenses which were not covered by insurance.

Changing the number in family or adding to Federal Taxes paid to reflect expenses provided to support family members who do not reside with the family but for whom significant cash support is provided.

While these are just a few examples of Professional Judgment, the list of what a financial aid office can do is almost limitless. They can change any individual FAFSA element they want if you provide a documented rationale with the relevant third-party documentation. Remember, they can do it, but you have to prove your case. You have to explain what makes your circumstance unusual and unexpected.

Hello all, and welcome again to 2020. I am sure many of you are heading into the Spring semester with new classes, new beginnings, and new opportunities for learning.

One of the new questions that has been circling around given the current world environment has to do with filling out the FAFSA and the military draft. Since there has been a lot of confusion about this, I thought I would add a few words of clarification here.

Filling out the FAFSA does NOT put you in the front of the line.

First, a reminder that we do not have an active draft. Remember we have an all volunteer armed forces (and we owe a great deal of gratitude, honor, and appreciation to those who volunteer for service). It would take an act of Congress to re-institute the Draft, and there is currently no move to do so.

Secondly, while registering for Selective Service is a requirement for men who are 18 years of age and older, and checking your status is a requirement for receiving Federal financial aid, there is no “priority” for those who complete the FAFSA. In fact, the information confirming your registration comes from a database match between the two systems (FAFSA and Selective Service) and no permanent record is maintained of this check on the Selective Service side.

So what is Selective Service? It is a system that guarantees that IF a draft is ever declared that all men ages 18 to 24 would be eligible for service. But again, this hasn’t been used since the Vietnam War and no one has suggested that the Draft would be restarted.

So now that we have put that issue to bed, let’s return to taxes. The first question you should be asking is do I have to file a Federal Income Tax Return? Generally if you are single, under the age of 65, and not self-employed (only paid by your employer through a standard paycheck), then as long as you earned less than 12,000 in 2019, you do not HAVE to file. a Federal Tax Return. If you are claimed by someone else as a dependent, you are married or self-employed (or both), or you have other special circumstances you should check with the IRS to see if you are required to file. The IRS has an interactive tool that can help you determine if you are required to file a return.

Just keep in mind, even if you don’t have to file a return, you may still WANT to file a return. Check your paystub or W-2; if your employer has taken out Federal Income Tax, the only way you can get this money back is by filing a tax return. And the amount withheld may make it worthwhile.

Especially because there are many free resources to help you file your taxes. More on this next time.

What paperwork should you have ready when it is time to file your return? First, make sure you have the W-2 forms from each of your employers for 2019. These forms show how much you earned for the year and how much Federal Income Tax was withheld. Note that companies might not send these to you until the end of January. You also want to make sure you have any 1099 Form for miscellaneous income (or self-employment income). Also make sure you have any other tax forms you might have been sent (like interest forms from your bank, or loan repayment forms for your education loans, and your 1098-T from your college for tuition paid).

We’ll get more into the filing process next time on the blog! Stay well!