Have you heard about the controversy sweeping the internet? Yes, that’s right. Someone rewrote the ABC song. You know, the one you sang as a child when you learned your alphabet? In order to make the letters more understandable, the new version changes the classic “lmnop” part to “lmn”. I know, mind blown!!! Check it out here and let me know what you think.

Is it really that bad?

I’m not sure that it is that bad, but it certainly isn’t the version I grew up with. But since we are talking alphabet, let me introduce you to some (perhaps) new letter combinations to you: COA – EFC = NEED.

What is that? And what does it have to do with financial aid? I’m so glad you asked.

COA stands for Cost of Attendance. The Cost of Attendance is an estimate of how much a year of education will cost for the average student at each college or university. Each school determines their own COA, and they may have several different versions of the COA depending on factors like living on- or off-campus, qualifying for in-state tuition, or going part-time vs. full-time.

The COA is not supposed to only represent the amount that you would pay the school directly if you were paying the whole cost of school. It is supposed to represent both direct costs (those you pay the school, like tuition and fees, on-campus housing and meal plans) and indirect costs (like transportation, books, off-campus housing and meals).

So, if you have your COA, the next important letters to know are the EFC (or Expected Family Contribution). In a previous section of the blog, I went through in great detail how we determine your EFC, but as a reminder here, keep in mind that the EFC represents an estimate of how much your family can absorb in college costs in a year. Again, no one expects you to be able to write a check for this amount, but rather this number represents your contributions from savings (if any) and current income based on the Federal formula.

The difference between these two figures, your COA minus your EFC, represents your NEED. This is the amount of need-based financial aid you can qualify for at the college. Each college will have a different COA, but you should have (approximately) the same EFC no matter which college you attend (*with a side note about private colleges who have money of their own to give away), so your NEED will be different college by college.

The way the financial aid system is supposed to work, though, your EFC should be the same school by school, so all that really changes in your COA and your NEED. This means that no matter which school you attend, your contribution (how much you and your family have to pay) should be the same.

Now there are many reasons this may not work in reality (maybe you applied late, maybe the college has limited resources, maybe your EFC is higher than the college’s COA so it appears that you are paying less), but generally this is the way the system works.

It’s a classic. No need to make a new version (unlike our new alphabet song).

We will be talking more about budgets and budgeting this month. Let me know if you have any questions about any of the topics, or suggestions for questions which are bothering you.

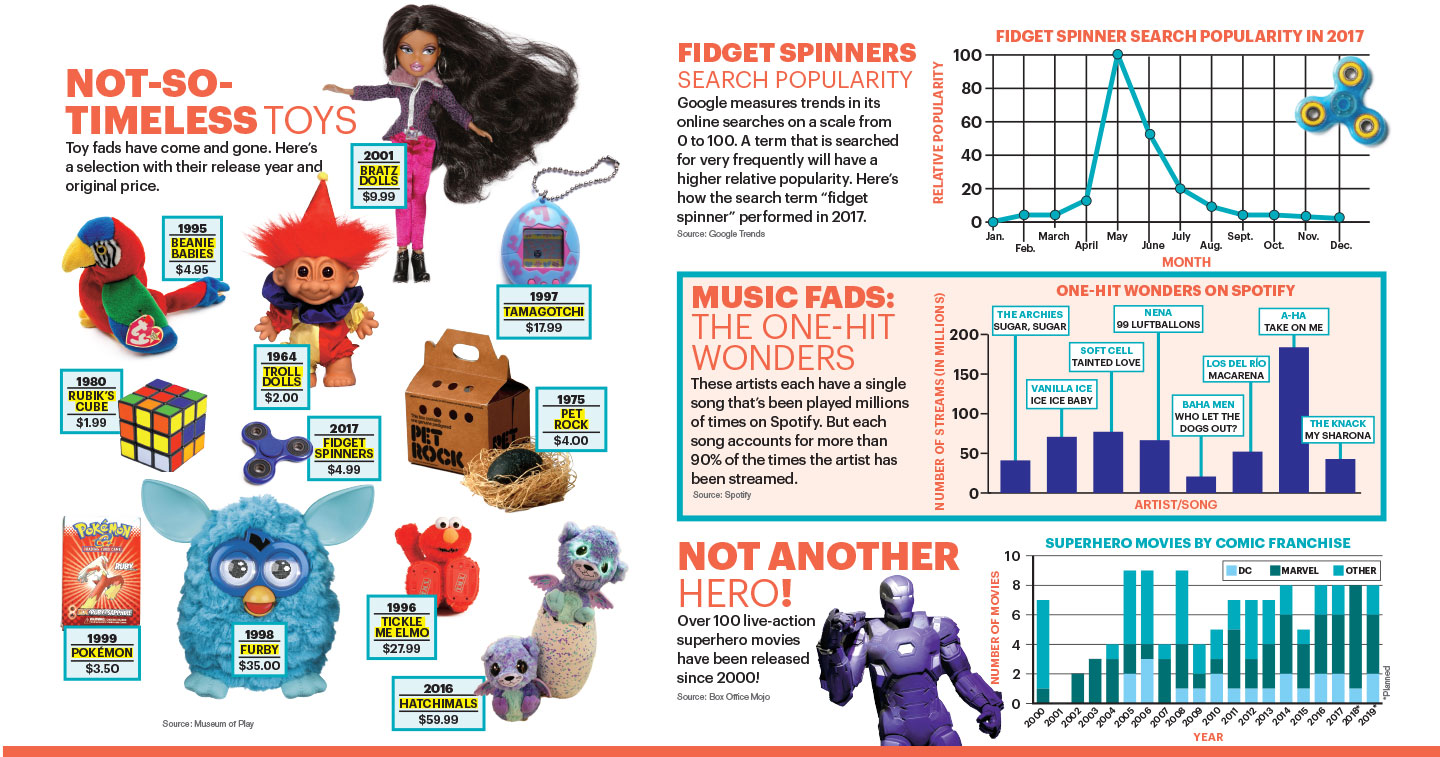

Are you the trendy type? Do you wear the latest fashion, have a presence on the latest social media app (I see you, Tik Tok), listen to the number one songs on the radio, see the latest movie? Trends are like that; they are the original memes where something hits and hits hard. And then in 1 year, 3 years, 5 years, 10 years, no one remembers them.

Rest in Piece Rubik’s Cubes, Pet Rocks, Tamagotchies, Fidget Spinners, Pokemon Go… you can fill in the blank.

It’s all so trendy…

Now don’t misunderstand me. Trends aren’t all bad. When everyone is focused on one product or idea, then that idea or product gains nearly universal acceptance. For a moment, everyone agrees that it is “in” (or “hot” or “cool” or “ill”). As you can see, even language can have trends!

So what does any of this have to do with financial aid? Bear with me, I’m getting there…

Every year, the College Board (yes, that College Board) releases several publications about college pricing and financial aid. You know about the College Board because of their work with the SAT, AP examinations, and – yes – the College Board’s CSS Financial Aid Profile, but I bet you’ve never seen their Trends publications. (See what I did there?)

I want to look with you at one particular table because I think it is really important to understanding how financial aid works, and how I manage this blog. This table visible below is Total Student Aid and Nonfederal Loans for Undergraduate and Graduate Students in 2017-18 and is expressed in millions on dollars adjusted for inflation.

If you look at the 2017-18 line in the chart, you will see some interesting things. First, who offers more grant or scholarship financial aid every year, the Federal government, State governments, Private sources (like scholarship agencies), or colleges and universities? Well, looking at this chart we can answer this. Colleges and Universities offer far more in grant and scholarship aid (in 2017-18, over $60 billion) than any other source (the Federal government offered $41.6B in 2017-18 and all states in the US combined only offered $11B combined).

Another important lesson from this chart has to do with student and parent loans. While it is certainly true that students and parents borrow a lot to support their own investment in higher education, it is not the primary source of funding for college. Even including graduate borrowing (represented by the Graduate PLUS in the table above), the total borrowing of students and parents in 2017-18 was $105.5B ($93.9B from Federal Loans and $11.6B from nonfederal loans). This represents less than half of the total money available for financial aid. Now, I am not arguing that this number shouldn’t be reduced (I would love more grant assistance for students), but I often hear people complaining that financial aid is all loans, and this chart shows that isn’t true.

As you look at this chart, what questions do you have? What do you find surprising? What information fits with what you thought about the national financial aid picture? Post your thoughts below.

Maybe you’ve completed your FAFSA, maybe you’ve already done the IRS Data Retrieval, and you are sitting back thinking “I am so ahead of this!” Life is great, right? Well, sort of. Let’s make sure you’ve remembered the other financial aid forms. (And for those of you who haven’t done your FAFSA, you aren’t too late — click here to review).

Kickin’ back? Not quite yet.

Remember that if your college requires the CSS Financial Aid Profile, you must complete this second application form in order to qualify for institutional financial aid. As I stated in an earlier blog post, the single largest source of grant-based financial aid is educational institutions (more than the Federal Government and more than State Governments), so you always want to make sure you complete whatever form(s) your college or university requests. More information on the CSS Financial Aid Profile can be found here.

Just in case any of you who are reading this blog are still in high school (or parents of a high school student), the next financial aid application you want to be sure to complete is your state’s scholarship or grant application form (if there is a separate one). We discussed this previously here.

The fourth form you need to be sure to complete is actually school-based. Each college or university may have its own financial aid or scholarship application form and you want to make sure you have completed that form. Here is where we discussed this last. Some colleges may have their own application form (online with another example here or here). Some have listings of scholarship opportunities available at the college, while others provide a bulletin board with links to outside scholarship programs. Check your college to make sure that you complete any requested additional form!

And finally, there are always more private scholarship programs and opportunities to consider. We’ve spoken about this process before too; read all about the best way to research and apply for outside scholarships here. The list of possible matches is long, but the rewards are great. We’ll talk more about private scholarships in a future post, but don’t forget to keep up to date with them!

So this title is really for the parents out there (or the older students, maybe). Anyone remember the Beach Boys classic “Help Me Rhonda”? Maybe we need to write a spoof called “Help me FAFSA”?

I’m not the Beach Boys, but I do have some suggestions on where to get help for your FAFSA.

Help me, Beach Boys!

If you are stuck and don’t know where to begin, the best bet is to begin by completing your FSA (Federal Student Aid) ID. The FSA ID is your electronic signature and for many students (and parents) this can be the hardest part of the process. If you have questions about the FSA ID, this link provides many of the common issues and problems and gives the answers for them.

Once you have your FSA ID (remember, the student needs one and – for dependent students – at least one parent needs one), it is time to complete the FAFSA itself. FAFSA is a free application and you should never pay someone to complete the FAFSA for you! If you do need help, you can get free help in the following ways.

Check with your local high school to see if they offer a high school financial aid night! Many local high schools have college nights (or college financial aid nights) where a local college representative will come to the school and talk about financial aid, answer your questions, and perhaps offer a FAFSA completion lab. You want to make sure that the person presenting at your high school is reputable (and not trying to sell you anything), so ask if they actually work at a college before you attend. Moneyman (that’s me) has presented at more than 300 of these nights, and they are a great way to learn the facts about financial aid and the FAFSA.

Check to see if your state or college is offering a “Form Your Future” event. Many local colleges offer free events, often titled “Form Your Future” or “College Goal Sunday“. The free events allow you to come to campus, get hands on help completing your FAFSA, and hear from practicing financial aid administrators. Valencia College (in Kissimmee and Orlando), as an example, titles their event “FAFSA Frenzy” and it is held this year on October 15, 17, and 24 (check the web page for which day on which campus).

Check out the free Florida Virtual Shines College Week events being offered by Florida’s Department of Education. This three day event (from October 28-30) offers a number of free online sessions each evening on Financial Aid and Admissions topics (and the best part is they are recorded for later playback). You never have to leave your computer to participate!

Of course, there is one more source! Moneyman is here to help!

Have you started your FAFSA? What questions have you run into? How can I help you complete the form?

With apologies to the Beach Boys, maybe you are singing this song:

Well since October first I’ve been thinkin’ ‘bout it in my head I come in late at night and in the mornin’ I just lay in bed Well, FAFSA you look so fine (look so fine) And I know it’s gonna take some time For me to do the FAFSA Help me get it finished today! Help me FAFSA Help, help me FAFSA Help me FAFSA Help, help me FAFSA Help me FAFSA Help, help me FAFSA Help me FAFSA Help, help me FAFSA Help me FAFSA Help, help me FAFSA Help me FAFSA Help, help me FAFSA Help me FAFSA yeah Get it finished today

In past years, I have made sure my child and I have logged into the FAFSA website and completed the FAFSA right on October 1 (the first day that the application opens, and the earliest the form can be done). But last night, our family did an Escape Game.

Orlando is the Escape Game capital of the world, and we love escape games. If you haven’t experienced one before, they are filled with mind puzzles, locks and hidden keys, things to solve, and fun exercises to puzzle your brain. We had an hour to solve the room, and we were done in 37 minutes. It was kind of like completing the FAFSA.

The FAFSA application is the puzzle you need to unlock so you can make it to college (or to graduate school, or trade school). By completing the FAFSA, you too can open the door to a new possibility. And I bet you can get it done in less than an hour (probably in less than 37 minutes).

So, tonight, my college-aged child and I are completing the FAFSA. Will you join us and complete yours too? The application opened yesterday and while many college’s deadlines are not for a while, you are always better having done your application early (the earlier the better, since some funds can run out and they tend to be awarded in order of application completion).

If you want more information on the FAFSA (and the other financial aid applications you need to complete), choose the category on the side of the blog entitled “Applying for Aid”. There are lots of posts there that will explain each of the different application forms which need to be completed.

And remember: while you may escape the room (and you might even be the president of the hair club for men), you can never escape completing the FAFSA (if you want financial aid for college that is).

Probably like many of you, I grew up watching Disney films. Perhaps, not like many of you, I remember that before the days of DVDs, streaming services and (dare I say it) VHS and Betamax tapes, the only way to see an older Disney movie was when the film was brought back into the theaters. Every couple of years, Disney would re-release a classic film so that a new generation could see it for themselves. There is nothing like seeing the original film on a large screen.

Well, luckily, Disney is doing it again with some of their princess movies in the run up to the Frozen 2 release. Right now, Beauty and the Beast is in theaters, and the film gives us today’s blog post title.

Don’t believe me? Ask the dishes!

The “grey stuff” has its place in the world of Financial Aid as well. Often there are situations in a family that just don’t fit within the “rules” established by the Federal government, and a financial aid administrator has to rely upon her Professional Judgment to make a decision about that particular case. In these cases, there is no easy decision, and each aid officer may make a different decision.

No place is this more true than in the case of Dependency Overrides. If you read my last blog entry, we discussed the differences between the standards for dependent and independent students. But sometimes situations fall into the grey.

Imagine a situation where a student lives with his grandparents, but has not legally been adopted by them and they do not have legal guardianship of him. Further imagine that the student is not in contact with his father, and his mother – who lives out of state in a residential substance abuse treatment program – has had a history of mental and/or physical abuse. In this situation while the “rules” would tell us that the student needs mother’s information, it is likely that a financial aid administrator would allow this student to be considered independent.

So how does something like this work if you are a student with an unusual circumstance? It all begins with filing your FAFSA. Even if you are unable to have your parent(s) complete their section of the form, you need to do your sections and when asked if your parents are able / willing to provide information, answer “no”. Your FAFSA will be processed (although it will be considered incomplete until you take the next steps).

You then need to send a letter requesting a dependency override to the college(s) you are considering attending. If you are applying to multiple colleges for admission, send the paperwork to each of them; only one of them will need to complete the override to allow your form to be processed, but the school you ultimately decide to attend will need to make this determination themselves.

What information should you send?

If the college has a Dependency Override form, submit that. Note that many colleges do not have such a form, or do not have it featured on their web page. If you do see such a form (like this example from the University of Central Florida) then complete it and follow the instructions. If you don’t see a form on the college’s web page, then contact the financial aid office and ask if they have such a form. If not they will provide instructions on how to submit this.

Write a letter of special circumstances. In almost every case, the financial aid office will want a letter from you providing information about your situation. This is not the time to withhold information, or be coy. You should provide as much information as possible in your own words as to why you are unable to rely upon parental support.

Provide a letter documenting your circumstances from a third-party. Your case for appeal will be stronger if you can provide a letter from someone in a professional relationship with you. Examples include (but aren’t limited to): a member of the clergy, a therapist, a guidance officer, a lawyer, a faculty member. The letter should be on letterhead, signed and provide contact information for the submitter. It also needs to document the case you are presenting (for example, stating that this individual knows that there has been a history of abuse or neglect). Note that a letter from your relative, friend, roommate, or someone else in a personal relationship with you is usuallynot acceptable.

Provide whatever additional back-up documentation you can, and the school requests. If the school asks for it, provide any other information you can supporting your request. This may include a copy of a lease, a letter from the person providing you housing, a copy of bill showing a different address from your parents, or any other documentation the school requires.

Note that Dependency Overrides are annual, so you will need to again establish your need for one in each year you are a student (or until you become independent for some other reason).

While this may sound complicated, every financial aid office provides a number of these overrides every year. Don’t let your relationship with your parents (or your lack of one) be a stumbling block to your qualifying for financial aid.

There is one condition, though, where a lack of parental “support” usually doesn’t qualify a student for a waiver, and that is a parent who is simply unwilling to complete the FAFSA. As I said in my earlier post, completing the FAFSA does not “obligate” a parent to pay for college; the FAFSA is simply a way to determine eligibility for financial aid. The Federal Government will not allow an override simply on the basis of unwillingness.

In the case where there is no mitigating situation, and a parent simply won’t cooperate, students do have one final option. If you are in this situation, you can submit your FAFSA without parental information but the only source of aid you will qualify for will be the Unsubsidized Direct Loan. This isn’t a terrible last option (it’s better than paying for college by credit card) but there are matters to consider when borrowing student loans (and we will get into that in a later blog entry).

So, now that you have tried some of the “grey stuff”, tell me — what questions do you have? What Disney movie is your favorite? And what memories do you have of seeing one in the theaters?

There is a running joke in financial aid. When asked a complicated question, a well trained financial aid officer will answer “it depends”. That’s it; that’s the joke. Not that funny, huh? More of a truth. Often in financial aid, the complexity of each situation means that there is no easy answer and that each answer is context dependent.

It always depends…

The issue of dependency itself is one with complications. What I mean by this is defining who is (and is not) a dependent student. Dependent students have to have their parent(s) fill out their financial aid applications, and therefore have their financial aid eligibility impacted by their parent(s) income and assets.

For Federal Student Aid, there are a few “rules” that determine if the FAFSA requires parental information. Here is a graphic that shows these rules (but keep in mind, it depends; more about this later):

So, if you read the graphic above, you will see that the following groups of students are automatically independent (as long as you qualify for one of those, you are independent):

Students 24 years of age or older.

Students enrolled in graduate (post-undergraduate) programs.

Students who are married or separated (but not divorced).

Students who have children for whom they provide more than 1/2 of their support.

Students who have dependents other than children who live with them and for whom they provide more than 1/2 of their support.

Students who are orphans, in foster care, wards of the court, who have a legal guardian (other than their parent), OR who are unaccompanied youth or homeless (or at risk of homelessness).

Students who are on active duty for the military.

Students who are veterans of the US armed forces.

Note that nowhere above does it say anything about being self-sufficient. So, let’s say you are a 22 year old who never went to college and who has been living independently from your parents since you graduated high school — you would not qualify for independence; we would still need your parents’ information for the FAFSA.

Also you’ll notice that nowhere about does it say what to do if your parent(s) refuse to fill out the FAFSA. The assumption is that your parents will be willing to do so. Here is where a number of parents / students misunderstand a basic principle:

Filling out the FAFSA does NOT obligate a person to pay for college.

The wise author of this blog…

The FAFSA is not like a mortgage application where you have committed to repaying (or paying) for college; it is more like an application for benefits. With a FAFSA you are seeing what funds you might be able to qualify for, there is no “obligation” to then accept these funds, or in fact pay. That comes later.

So, let’s say your parents simply won’t fill out the FAFSA. Or you aren’t in a relationship with your parents, but you are under 24 and don’t otherwise qualify to be independent. What do you do then?

Check out my next entry on the blog to see what options you have!

The school year has begun as all over the country students are back in classrooms, the traffic is backed up with school buses and the temperatures have begun to cool (although, sigh, not really in Florida).

The School Year Begins

Another aspect of the start of the new year is the beginning of the financial aid and admissions application cycles for those of you who are seniors in high school (or adults thinking of going back to school, or students thinking of going to graduate school). Now is the time where you are beginning to think “what’s next?”, when your parents, friends, neighbors and guidance officers ask you for the names of colleges you are thinking about, and when you are faced with the question (that honestly never goes away) of “what do I want to be when I grow up?”

As you think about your college plans, it is natural that one of the areas of concern is money. Money plays an important part in your college decision process, but the good news is that if you follow the plans outlined on this blog, and the advice of your guidance officers and others, money doesn’t have to be the deciding factor for you. If the system works, you should be able to decide upon the best college for you based on fit, not on finances.

Over the past several months, I have been busy helping students at my school get ready to start their school year. Now that their enrollment has begun, I plan to turn my attention to this blog and helping you — whether you are a senior in high school, a parent of a student, a student currently in college, or just an interested adult — learn about college financial aid, about money management, and about how best to make the system work for you.

So here is my question for you. Who are you? I want to make this blog a conversation with you. Sure, I like to talk; I like to write (I am a published poet and I was voted “most talkative” as my high school senior superlative), but I prefer to have a dialogue. A conversation is much more interesting to me than a monologue.

Tell me what you want to know? As I target at least one blog entry each week, what would you like me to focus on? What questions do you have about the college process? How can we best learn together?

Welcome to the Fall… to pumpkin spice and maple frosting… to jack-o-lanterns and apple cider… to crisp nights and color-changing leaves. And welcome to the Moneyman College Financial Aid Blog where we learn about college financial aid together.

So, much earlier, I began a post about how we determine your family contribution. I started the conversation by describing the four parts of the contribution and discussed how there are really two methodologies used, one for Federal funds, and one for colleges who use the CSS Profile to determine eligibility for their funds.

Next, in two separate posts, I described how the two methodologies handle Parent Income, and Parent Assets.

This post will attempt to address the last two components, the Student Contribution from Income and the Student Contribution from Assets. (Note: this information applies to dependent students only and does not apply either to independent students with or without dependents. If you are unsure as to your dependency status, check out the first post above for some definitions).

It’s All About the Money

When examining student income, we begin at the same place we began on the parent side – with the Adjusted Gross Income from the the base tax year (in the case of students attending in 2019-20, that would be 2017). We add to this any nontaxable income (such as tax-exempt interest, IRA contributions for the current year, tax-deferred contributions, etc). We also subtract out from the income any taxable financial aid which is included in the AGI (this might include Federal Work Study earnings from the previous year or scholarships that were taxable in the previous year).

As with the parent income calculation, there are several items which

are removed from the student income as allowances against the income:

US Income Taxes paid — Again, this comes directly from the tax return.

State and other taxes — Again, a percentage of the total income (as determined above). This percentage is determined from two sets of tables, one for the Federal Methodology and one for the Institutional Methodology. As with the parent tables, the IM values are more generous than the FM ones.

FICA Taxes — Based on wages earned, a 7.65% allowance representing Social Security taxes.

Income Protection Allowance (for FM only) — An allowance used in the FM formula against the income representing student costs of living (for FM in 2018-19 the number was $6,570).

Student available income is determined by subtracting the total of the allowances from the total income. In both the IM and the FM formula, this value is then multiplied by 50% to indicate that there are other expenses that students have (but note that this percentage is much higher than the parent conversion rate).

Some institutions (mostly private high-cost colleges) have minimum student contribution levels that they set which reflect the expectation that students will earn money during the summer before the school year begins. Different colleges have different minimum levels and different policies about excess earnings, so you really need to talk to each of them to find out their policies.

An important note about the student IPA though is the high level (relatively) of the standard deduction. Having a $6,570 IPA means that a student has to have earned more than $6,570 after Federal, State and FICA taxes before any of their income would be counted in the contribution. This is a higher than many students would normally earn.

Now on to student assets. Here it is actually fairly simple.

We take into account the same assets for students as we did for parents. Namely:

Cash, savings and checking accounts.

Non-retirement based investments (including trusts).

Real estate owned by the student (don’t laugh).

Home owned by the student (don’t laugh harder — and by the way, home is only considered in IM, not FM).

Business or farm equity (and remember this is also adjusted like the

parent one was, somewhere between 40 to 60% of the equity depending

upon the amount of the equity).

Once the total asset value is determined, the FM formula says to take 35% of the value and include that in the Student Contribution. The standard IM formula says to take 20%. As you can see, this is a MUCH different treatment than parent assets (which have a much lower assessment rate).

The 568 schools use a different approach. We combine student and parent assets as family assets and subject them all to the parent analysis. This hopefully alleviates the concern that students saving in their own name are penalized for this. For these schools, they believe savings should be treated uniformly. They try to address this in our approach.

So, now I have addressed all of the components of the Family Contribution and how we determine them. Next up, information preparing you for your award notification!

I know it has been quite a while since my last post. Tax day has come and gone, and here we are the Spring holiday season. As we enter a time of rebirth and new beginnings, it seemed an appropriate time to return to the blog.

On to my second post on the topic of how we determine your family’s contribution. The first post was on parent contribution from income. This post will be in regard to the parental contribution from assets.

There are lots of kinds of assets… ===

There are some assets that are included in both the IM (Institutional Methodology – used by schools to award their own money) and the FM (Federal Methodology – used to award Federal funds) formulas. These include:

Cash and savings accounts.

Stocks, bonds, mutual funds, and other regular (i.e. non-retirement) investment accounts (including life insurance cash value).

Real estate other than your primary residence (including investment real estate, 2nd homes, etc).

Businesses or farm equity (this amount is not at a 100% assessment rate, you report the total amount on the form and we make an adjustment based on a table, usually somewhere between 40% and 50% depending on the amount of equity). Special note: Businesses not owned by your family OR that have more than 100 employees are included; others are ignored. In order to determine what makes up your business or farm equity, some colleges may require a business or farm supplement for each business you own (this may include a Schedule C, Schedule F, Partnerships, S-Corporations, and regular Corporations tax returns).

Some assets are ignored from both formulas. These include specially designated retirement accounts like 401K accounts, IRAs, KEOGH plans, etc (although remember the amount of the current year’s contribution was added back as non-taxable income before).

One particular asset is included only in the IM formula, and not in the FM formula. This is the home, or the primary residence. Some colleges may use a number of modifications to your reported information to arrive at a reasonable value while other may use your entire home equity as an available asset, so you may want to confirm with the institution what policy they have in place.

Why is the home not included in FM? In 1993-94, the Federal Government removed the home from the financial aid formula. This was done for several reasons, I believe, none of which make particular sense from the point of view of assessing a family’s ability to pay for college. The action of removing this asset from the formula was to, in effect, pretend there is no difference in a family’s financial strength whether they rent an apartment or own their home. Private colleges determined that this analysis wouldn’t work for them, so they created their own process to analyze financial aid (therefore the birth of the Institutional Methodology). There are very many other differences between IM and FM, but the issue of home equity serves as the starting point for their divergent paths. A history book on this subject is just itching to be written…

So enough history, what does colleges actually do?

Some start by looking at what year you purchased your residence and how much the purchase price was in the year in which you purchased it (I say you when in fact, more than probably, it is your parents’ house). Based on a table which eliminates regional variation, they may determine how much the property should be worth today. This table uses a national coefficient so that parents are neither penalized or advantaged by living in an area where values over time have deviated from the national norm. The chart is is not publicly available. The underlying information comes from here though.

Once the college determines the value as shown by the multiplier, they may compare that to your stated value (on the Profile application) and in some cases they will use the multiplier value (or they may use your stated value on a case-by-case basis, usually if it is lower than the multiplier value).

The next item some colleges examine is whether you could access the value in your home. To determine this they cap the total value based on your total income. Let’s say the cap is 240%. So, a family who earns $100,000 a year would have their home value capped at $240,000. In other words, a collge using a 240% cap would cap your home value at 2.40 times your income. This is to protect families who, due to real estate market growth, live in a home that they could not afford to purchase today. The college caps the value of the home at this amount to account for the fact that a family could not afford to qualify for a mortgage to access equity higher than this level.

The college then takes the lower of these two numbers into account as your total home value, and then subtracts debt from that to determine the home equity. Again keep in mind all of this is an example of what a college may do to award their own money. Colleges must use FM (which does not include home value) for Federal funds.

Another asset some colleges consider under IM is the student’s siblings’ assets since they try to get a whole picture of a family’s net worth (they will also later provide an allowance against these assets for the siblings’ savings for college). In addition, under IM, colleges may consider all student assets (with the exception of trusts) to be family assets as well so that students will not be penalized for saving for college (due to the higher rate used in the student-only analysis).

Once all of your assets are in place, the college then subtracts allowances from them to determine your net worth. The allowances are different depending on the formula.

The following allowances are subtracted under the FM formula:

Education Savings and Asset Protection Allowance — An allowance against assets based on the age of the older parent and marital status. As an example, for a married couple with an older parent aged 48, the amount is $21,300. For a one-parent family with a parent aged 48, the amount is $12,900. This amount is supposed to be, according to the Federal formula, a protection against your assets to supplement your retirement and to allow for savings for college for younger siblings of the student.

The following allowances are subtracted under the CA formula:

Emergency Reserve Allowance — An allowance against assets based on the number in family and in college (modified by a regional COLA – Cost of Living Adjustment – figure) to represent what a family should have saved in case of emergencies.

Cumulative Education Savings Allowance — An allowance representing how much a family should have saved by this point for college for this student as well as any college-attending or younger siblings. This amount is based on an Annual Education Savings Allowance calculated earlier in the formula.

Low Income Asset Allowance — If the Available Income calculated before is negative, the amount is subtracted from assets available (to represent that the family is living off of its assets).

The resultant value (Net Worth minus Total Allowances) is then referred to as the Discretionary Net Worth. Discretionary Net Worth is then combined with Available Income and the whole thing is run through a final conversion, leading to somewhere between 22 to 48% of Available Income (based on how high the Available Income is) and somewhere between 3 to 8% of Discretionary Net Worth (again, based on how high the Net Worth is) appearing as part of the final contribution from parents.

This figure is finally adjusted to reflect how many students are attending college in the same academic year. Under the Federal Methodology, the number is simply divided by the number in college (so, if your contribution was $10,000 and you had two in college, each student would have a $5,000 parent contribution).

Under the IM methodology, the resultant number, instead of being evenly divided, is modified by a percentage (60% for two in college, 45% for three in college, 35% for four or more in college); this would mean that for a contribution of $10,000 with two in college, the contribution for each student would be $6,000).

So, I think this is a good general overview of the asset treatment. And here I thought this would be simple. Ask away, since I am sure this will generate questions.

Again, please let me know if this is way too much detail, or not enough information.